The government need to treat investors and developers as the solution, not the problem. Supply is the long-term solution – and it comes from developers and investors. You need both.

The investors buy the assets from the developers. If the government continue to make it too hard and annoy property owners (the “landed gentry”) with uncommercial tenancy laws and rifle taxes on property (e.g. interest non-deduction, which is manifestly unfair), then the housing crisis gets worse, not better, because as an industry we will increasingly sit on our hands and wait for a more commercial government.

Instead of vilifying and blaming property investors to deflect the issue away from government, I suggest Labour, academics, and the like do the following:

1. Stop worrying about what investors get, and look at what they actually do for NZ. They supply and manage housing, an essential service. They are one of your most important suppliers. Look after and help them, and you will get more supply. If you really encourage supply with good zoning and infrastructure on tap, you will see developers build too much stock and oversupply the market. (Arguably this is happening in Auckland at present.) Oversupply is the answer to the government’s problems: rents drop and so do house prices. Everyone gets a house.

2. Stop disrespecting investors. You get no respect or buy-in from our industry by pelting us with insults and labels; you just look like envious socialists playing the blame game. And the attitude pervades through public policy. Creating scapegoats (investors) for what is a problem caused by successive governments’ under-investment in housing, is nasty. Calling us tax cheats, alleging our “real motivation” is untaxed capital gains, demonstrates the government does not understand investors’ business model and intentions at all. (We can’t retire on capital gains; we retire on cashflow, which is taxed.) If you really can’t live with the gains being untaxed, then damn well step up and go to the election on a CGT platform; get permission to do it.

3. Instead, make it easier for developers and investors to succeed, and you will get more supply.

a. Immediately seek consultation with our community on how you can assist us to solve the housing supply problem.

b. Immediately look at how successful the Auckland Unitary Plan has been at reducing land costs in Auckland, by allowing multi-unit sites and high density housing. (Splice a million dollar section into 10 units, replacing one McMansion. Land cost dilutes 90%, houses get cheaper.) All cities and towns across NZ need this zoning change now. I know developers building to rent, and the zoning rules in small towns and most cities come from the 1960s, where everyone gets a quarter acre section. Times have changed; zoning needs to keep up.

c. Immediately assist landlords with rolling back the no-cause 90 day termination notices you abolished. This makes it nearly impossible to manage anti-social tenants, and makes me (and others) very, very picky with tenants, amplifying your emergency housing problems. Do they not see the link?

d. Continue to ramp up and forward-fund infrastructure. (Brief accolade here to Labour. They inherited a hopelessly rundown national infrastructure from successive National and Labour governments’ under-investment in housing infrastructure. They have pledged $3.8b to infrastructure, and more, and it’s already helping small towns and cities. I’ve seen it first-hand.) Keep doing this and spend more building sewers, stormwater, telecommunications, and all infrastructure. Upgrade roads and public transport. This is the best investment in the future of NZ housing supply.

e. Don’t charge developers a development contribution that exceeds the cost of their actual pro rata share. All this does is encourage developers to land bank and sit on the land undeveloped because they feel like they are being taxed through the back door with exorbitant development levies. If you want supply, do what they did in Australia and forward-fund the 20 years of future development infrastructure. Charge developers a pro rata and fair connection fee as they connect to the infrastructure. There is talk at the moment of doubling development levies and there’s consultation going on about it. Quite simply, if this happens, many developers will just sit on their hands, and this will undermine supply. Moreover, developments that do proceed will simply pass the cost on to the buyers. Government needs to socialise the cost of forward funding, with a long-term scheme socialising the cost over the total potential number of connections. Not slam the current developers in a tax grab.

f. Stop with infusing ideology into Resource Management Act reform. It seems the government’s main agenda coming out of their initial work in this area is implementing He Puapua and Iwi rights into land development and the environment concerns. I thought this reform was about cutting red tape? They have lost perspective here.

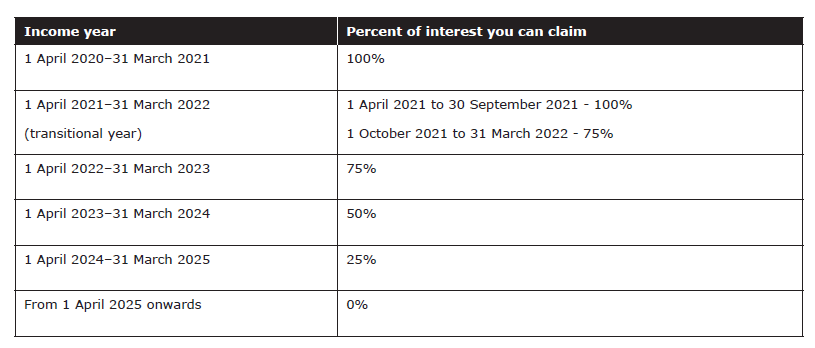

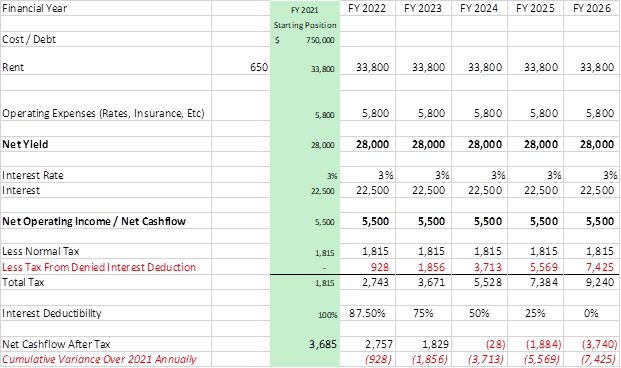

g. Repeal interest non-deductions. Otherwise, when interest rates go up, you will send cashflow poor investors broke. This is because a rise in interest rates will no longer trigger tax relief, smashing the cashflow of fixed income households. The damage that will be done to supply by taxing the net yield (i.e. income before interest costs), rather than the net cashflow, won’t be seen until the phased in non-deduction rules bite in the 2025 and 2026 financial years, 3-4 years away. A downturn like this will inevitably stall investment in housing and reduce supply.

h. Understand that the rough end of the tenant pool is now toxic to private investors, due the removal of the no cause tenancy termination. Labour made this rod for the government’s back because they don’t understand the housing market. Their emergency housing demand is blowing out. One of the reasons is because landlords are under-supported in the tenancy tribunal, and now without the ability to remove a tenant with ‘no cause’, most landlords won’t touch tenants with social problems. It’s just too hard. So it rebounds on to the government and will continue to do so, until tenancy laws are made more commercial. This is directly caused by these tenancy rules. I speak from listening to clients.

There is no one simple or specific cause to problems of housing affordability, lack of supply, and wealth inequity. But it’s obviously not tax that causes all these problems. It’s cheap money, loose lending practice, and a desire to benefit from leveraged gains, which unleveraged investments (like stocks)