Extension of the bright-line period

Currently the bright-line period for residential property is five years. For residential properties acquired on or after 27 March 2021 that period will increase to 10 years. There is a a significant exception to this rule for ‘new builds’, which will continue to be subject to a 5-year period. There is not a lot of detail on what a ‘new build’ is, although the suggestion is that it will include properties that are acquired within a year of the Code Compliance Certificate being issued.

A key question here is what constitutes ‘acquisition’, which is critical for determining if the 5 or 10 year rule applies. Acquisition occurs when there is a binding sale and purchase agreement in place. Thus if your agreement is dated prior to 27 March 2021, then the 5-year rule applies. If the agreement is dated on or after 27 March 2021 then the 10-year rule will apply.

An immediate point for readers to be aware of is that if you are considering restructuring the ownership of an existing property then you need to have a binding agreement in place to sell it into the new entity before 27 March 2021, if you want the new entity to be subject to the 5-year bright-line rule rather than 10-year rule.

There is also a change to the main home exemption. Previously you got this if you lived in the home for most (i.e. more than 50%) of the time that you owned property. Under the new 10-year rule, you only get to claim the main home exemption in full if you have lived in the property 100% of the time. If the property has been used as your home for part of the time and as a rental for part of the time, then the gain that arises on sale is apportioned across the relative uses and you pay tax based on the proportion of the time that it was not your home.

No interest deductions

This is a more significant change for investors and was not signalled by the Government.

From 1 October 2021 there are going to be restrictions on residential property investors’ ability to claim interest as a deductible expense. For properties that are not new builds and acquired on or after 27 March 2021, you will not be able to claim any interest deductions at all.

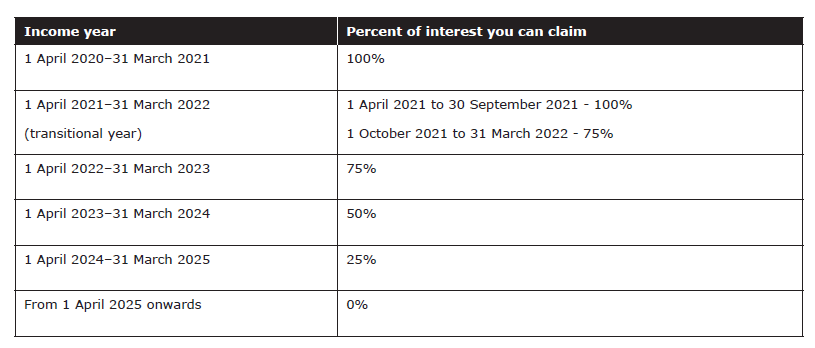

For second hand properties acquired prior to 27 March 2021 your ability to claim interest will be phased out over the next four income years, so that from 1 April 2025 there will be no ability to claim any interest as a deductible expense against residential rental income. The phase-in period over four years sees interest become progressively less deductible over each financial year as depicted in the following grid:

Interest incurred on a ‘new build’ that is bought for investment purposes is exempt from this, i.e. interest deductions can still be claimed where you buy a new build as a rental. The question is though, what ‘new builds’ qualify for such exemption? This is yet to be clarified and the Government have given themselves up to 1 October 2021 to work out what this definition is. They have said they will consult as part of the process.

Interest incurred by property dealers and developers, is not impacted by this change, i.e. still deductible. Obviously, property dealers and developers pay income tax on profit realised when the property is sold.

Under current rules, which have been in place for decades, you get to deduct interest against rents – 1/3 of interest is therefore tax offset. With no tax offset between interest and rent, you now pay effectively 33%-39% of the interest not deducted. (Assuming you are paying tax at 33%-39%.)

For instance, if you previously received $32,000 in rent and paid $5,000 in rates, insurance and repairs, and $27,000 in interest, you had net cashflow of zero. Now you will have to pay tax on $27,000, due to interest not being deductible. So net cashflow will become negative $9,000 due to the new tax rules, when previously it would be zero. (At 33% tax).

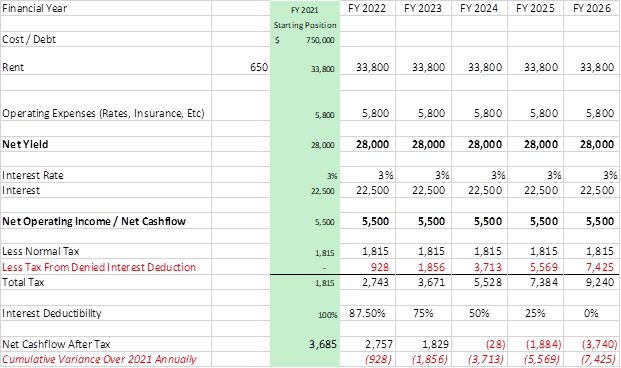

Illustration of phasing in of interest deduction changes

Have a look at the table below which shows how these changes will affect an investor as they are phased in over four years. In this example, the investor has a $750k property, with $750k of debt at an interest rate of 3%.